Energy Regulation Solutions offers specialized regulatory consulting at the intersection of innovation, climate goals, and market readiness. We support developers, investors, and policymakers in navigating complex regulatory landscapes for hydrogen, CO₂, and Power-to-X technologies in the EU, Germany, and the US

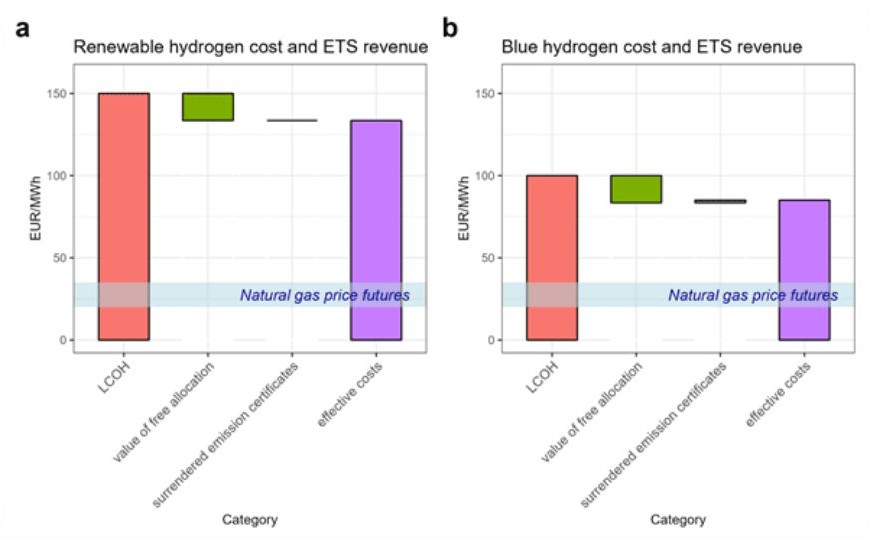

Figure: Comparing green (left) and blue hydrogen (right) costs accounting for EU ETS impacts (assumed CO2 price: 80 €/tCO2) based on the optimistic end of near-term cost estimates for 2025 to 2030. The value of free allocations is calculated based on CBAM factor of 100 %, which applies until the end of 2025. No additional subsidies considered here.

Hydrogen in the Reformed EU ETS: What It Means for Competitiveness and Emissions Reductions?

🔹 Key insights:

📌 The EU ETS alone cannot make hydrogen competitive.

Hydrogen production (both renewable and blue) remains significantly more expensive than natural gas — currently 4 to 6 times more costly.

The value of freely allocated ETS allowances does little to close this gap, as illustrated in the picture below with the green part, especially with today’s relatively low CO₂ prices.

📌 To bridge the cost gap and enable a fuel switch from natural gas to low-carbon or renewable hydrogen, CO₂ prices of €300–500/tCO₂ would be necessary.

📌 Switching from blue to green hydrogen would require €2500/tCO₂ if only downstream emissions are priced.

✅ Policy recommendations include:

📌 Expanding the EU ETS to cover upstream emissions for a more accurate climate cost signal.

📌 Gradually lowering the emission intensity threshold (currently 28.2 gCO₂eq/MJ) for low-carbon hydrogen to encourage innovation and deeper decarbonisation.

💡 To use hydrogen for the energy transition, it is essential to go beyond emissions pricing and rethink how to support its competitiveness and climate impact.

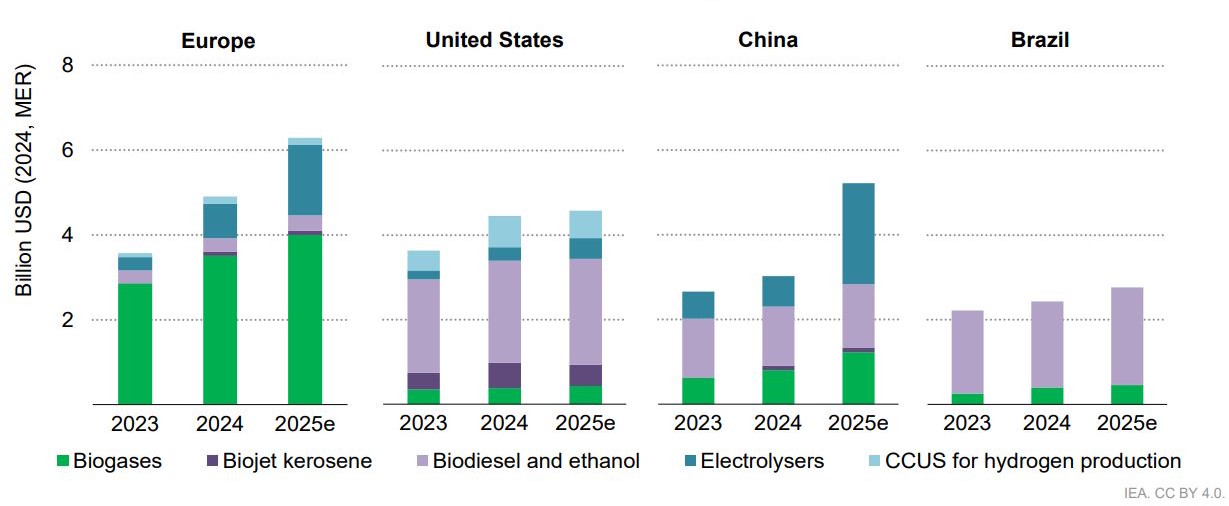

Investment in liquid biofuels, biogases and hydrogen is set to rise by 30 % in 2025, to nearly $25 billion, building on a 20 % rise in 2024.

📌 Low-emissions fuel spending varies greatly by region:

in 2024, Europe accounted for 60% of global investment in biogases;

the US made up 70% of global investment in biojet kerosene;

China has large investments in hydrogen;

Brazil focuses on liquid biofuels.

📌 Investment in liquid biofuels, biogases and low-emissions hydrogen is set to rise by 30% in 2025 to a record high close to USD 25 billion, building on a 20% rise in 2024.

📌 Policies and regulations remain essential to this growth: mandates, quotas and other forms of policy support have underpinned the high levels of investment in biodiesel and ethanol in the United States and Brazil and in biogases in Europe.

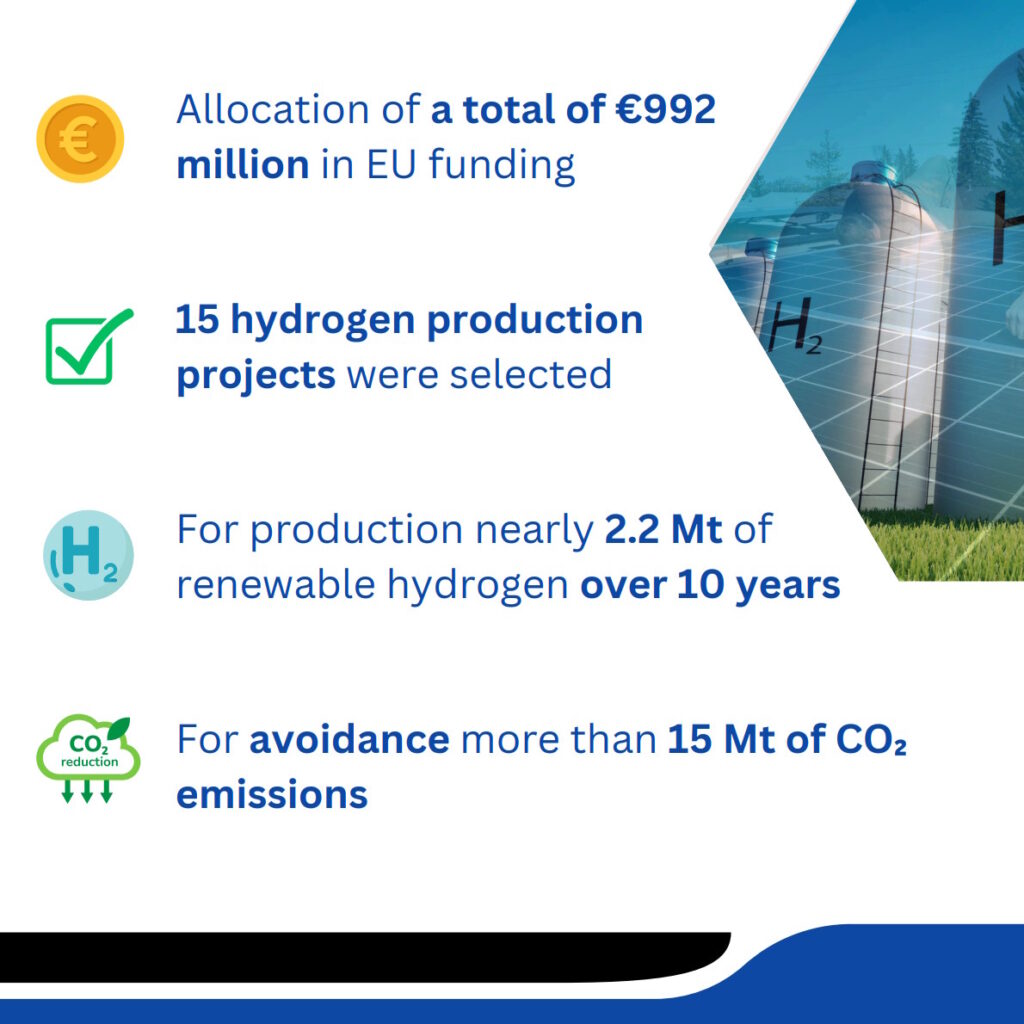

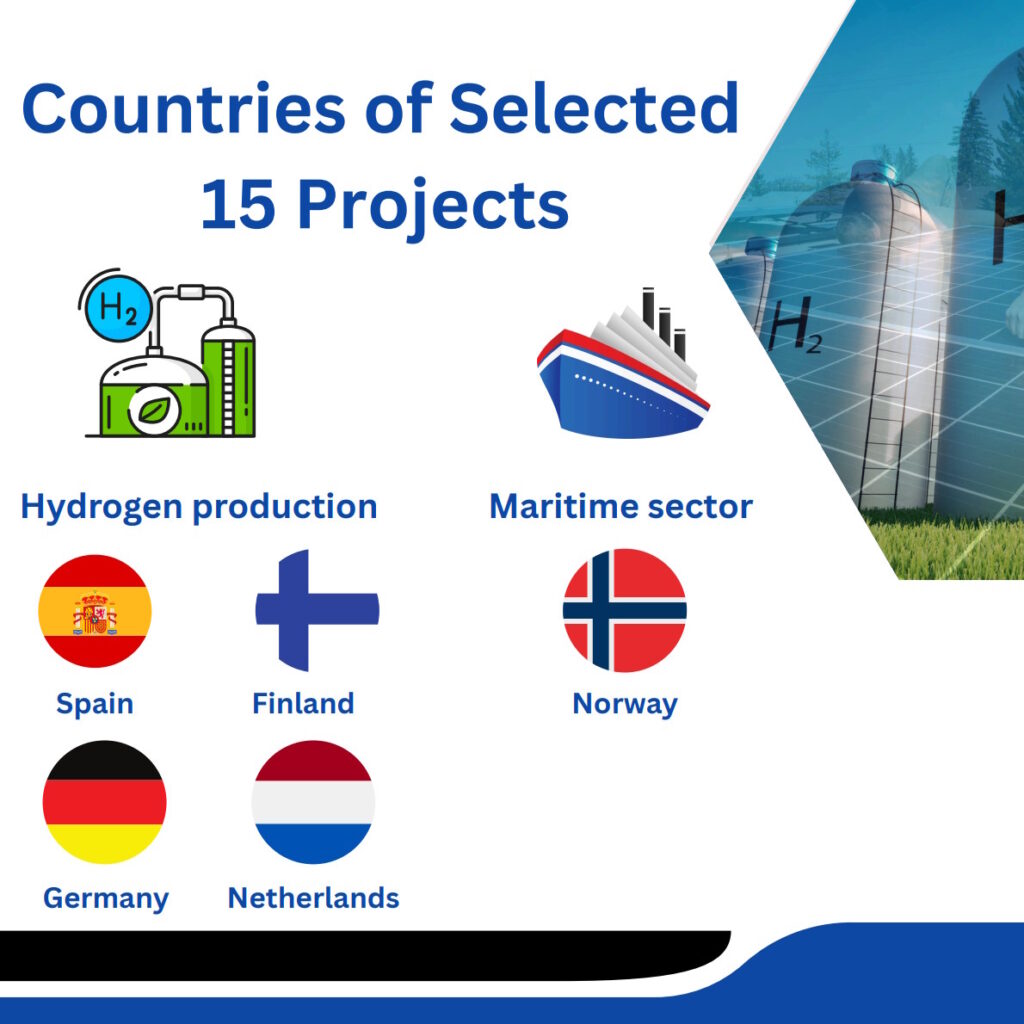

📌 Some hydrogen projects have been cancelled or delayed in the past 12 months, but there remains a pipeline of projects that have received FID, requiring around USD 8 billion of investment in 2025, a 70% increase from the level in 2024.

📌 For hydrogen:

there were a number of setbacks for projects around the world, nonetheless, investment rose by 60% in 2024, and there remains a large pipeline of hydrogen production projects that have received FID.

government support has continued in 2025 globally, for example, in Australia and the EU.

all hydrogen projects that have received FID would require investment almost USD 8 billion and would increase capacity to around 7.5 Mt in 2035.

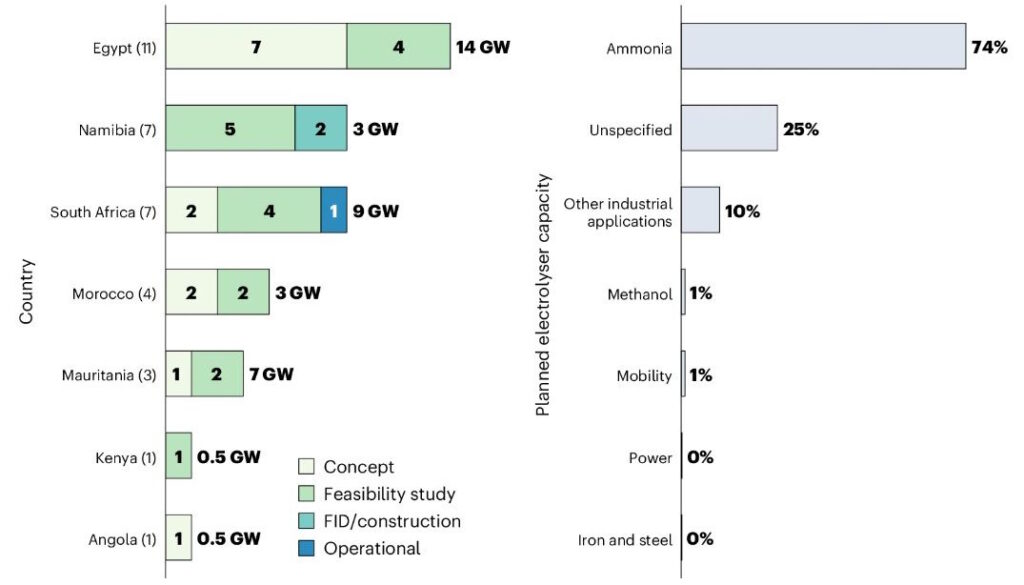

📃 Article “Mapping the cost competitiveness of African green hydrogen imports to Europe” was published by researchers of the Technical University of Munich (TUM), the University of Oxford and ETH Zurich.

✅ The Key Findings:

📌The research covers:

all projects planned to be operational by 2030.

the analysis of African countries with port access.

31 countries, except Somalia and Libya, were excluded due to political instability and small island states.

📌 Overview of African green hydrogen projects:

34 projects are found across 7 countries;

89% of projects are either at concept or feasibility stages;

2 of the projects have reached a financial investment decision and are under construction, and only one small-scale project (that is, 3.5 MW) in South Africa is operational;

From 3.5 MW to 6.9 GW is planned project sizes;

74% of planned electrolyser capacity is intended for ammonia (NH3) production

📌 Levelized cost of hydrogen (LCOH):

In a high interest scenarios 1 and 2, least costs for green H2 exported from Africa are €4.9 kgH2−1 without policy support and €3.8 kgH2−1 when fully de-risked by European governments.

In a low interest scenarios, the costs come down to €4.2 kgH2−1 and €3.2 kgH2−1, respectively.

no location competitive with the first round of auction results by the European Hydrogen Bank, which yielded a lowest bid of €2.8 kgH2−1 in Spain.

📌 Challenges:

many low-cost locations are in regions that are either politically contested or encounter relatively regular flares of armed conflict.

the size of the planned investments relative to the GDP raises questions on feasibility. This situation is concerning as many African countries face massive foreign debt burdens.

whereas wind resources are critical to low-cost green H2 production, local expertise to install this wind capacity may be insufficient.

some low-cost locations, such as those near the Red Sea or the river Nile in Egypt, may also face challenges of water insecurity potentially disrupting consistent production.

✈️ The International Civil Aviation Organization (ICAO) updated the dashboard with publicly-available information on sustainable aviation fuel (SAF) offtake agreements.

📌 This dashboard covers various locations worldwide.

📌 Volumes refer to neat SAF; in case of blended SAF announcements the volumes refer to the fraction of SAF in the blend.

On April 10, 2025, the Government of France announced the update of the National Hydrogen Strategy.

📃 The full text of the updated strategy is available via this link.

✅ Key Changes and Measures:

📌 Electrolysis installation targets in the region with up to 4.5 GW targeted for 2030 and 8 GW installed in 2035;

📌 Mastery of all hydrogen equipment and technologies throughout the value chain;

📌 The deployment in France of low-carbon hydrogen transport infrastructures within hydrogen hubs;

📌 Ensuring that the necessary framework conditions are in place for the development of the French hydrogen industry, particularly in terms of access to land, procedural deadlines, the development of a comprehensive, clear and stable regulatory framework, and electrical connections;

📌 A €4 billion support mechanism for low-carbon hydrogen production to ensure that low-carbon hydrogen is competitive with fossil hydrogen over 15 years;

📌 The relaunch of the ‘IDH2 Hydrogen Technology Building Blocks’ call for projects, designed to support the development of certain critical elements of hydrogen technologies;

📌 A new call for projects for the deployment of hydrogen-powered commercial vehicles, to enable the technological development of fuel cells and tanks;

📌 Measures to support studies of synthetic fuel projects in order to bring about, by 2030, the first industrial production of synthetic fuels for aviation and maritime sectors.

On 23 May 2025, the European Commission adopted new pieces of secondary legislation and a communication relating to the Net-Zero Industry Act (NZIA).

📃 Adopted Acts:

✅ Communication providing updated information to determine the shares of the EU supply of final products and their main specific components originating in different third countries under NZIA

provides information on where the EU’s supply of net-zero technologies comes from, highlighting third country dependencies for specific technologies. This information enables the application of the ‘resilience’ non-price criterion in public procurement, renewable energy auctions, and other public interventions.

helps Member States in evaluating net-zero technology manufacturing projects eligible for strategic project status.

✅ Implementing Regulation specifying the pre-qualification and award criteria for auctions for the deployment of energy from renewable sources

These criteria include responsible business conduct, cybersecurity, and sustainability and resilience contribution.

Starting on 30 December 2025, the new rules must be applied to 30% of auction volumes (or 6 GW per year per EU country).

✅ Delegated Regulation regarding the identification of sub-categories within net-zero technologies and the list of specific components used for those technologies

replaces Annex with list of final products and specific components in NZIA.

✅ Implementing Regulation regarding the list of net-zero technology final products and their main specific components for the purposes of assessing the contribution to resilience

includes Annex with list of net-zero technology final products and their main specific components for the purposes of assessing the contribution to resilience.

✅ Implementing Decision adopting guidelines for the implementation of certain selection criteria for net-zero strategic projects

ensures a consistent selection process across Member States, through guidance on the applicable criteria for that strategic project selection.

☑️ What next?

📌 For the Delegated Regulation, following publication, the European Parliament and the Council have a 2-month scrutiny period (extendable by a further 2 months if requested), during which they can object to this act.

📌 However, there is no scrutiny period for the Implementing Regulations adopted on 23 May 2025.

On May 22, 2025, the U.S. House of Representatives passed “The One, Big, Beautiful Bill” (Bill) — legislation that proposes significant changes to energy-related tax incentives originally introduced under the Inflation Reduction Act.

➡️ Key Changes for Hydrogen:

❌ The Clean Hydrogen Production Tax Credit (IRC §45V) would be terminated for facilities that begin construction after December 31, 2025.

✅ The Clean Fuel Production Credit (§45Z) — supporting the production of low-carbon transportation fuels including hydrogen — would be extended from December 31, 2027, to December 31, 2031.

☑️ What’s Next?

The Bill now moves to the Senate, where further amendments are expected.

Final passage timing remains uncertain — but August appears more realistic than the previously anticipated July 4 timeline.

On 16 May 2025, the European Commission published its Opinion (C/2025/2004) on the statutory documents of the European Network of Network Operators for Hydrogen (ENNOH) – the independent association representing future hydrogen transmission network operators at EU level.

✅ Key Takeaways:

📌 Climate Objectives: the Articles of Association (AoA) of the ENNOH should be modified as to include climate related objectives.

📌 Membership Criteria: Only certified Hydrogen Transmission Network Operators (HTNOs) — or those undergoing certification — can be members. The “founding member” concept must align with EU law.

📌 Observer Access: Observer status should be restricted to HTNOs from countries applying EU energy law (e.g., EEA or Energy Community members).

📌 Board Composition: Rules must ensure regional balance while rewarding early movers — but with transparent limitations and future revisions.

📌 Stakeholder Engagement: Public consultations must be transparent, inclusive, and allow a default period of 2 months.

📌 Amendments & Dissolution: Changes to ENNOH’s statutory documents — including its list of members — and any dissolution must receive explicit Commission approval.

📌 Gender & Diversity: ENNOH is encouraged to integrate gender parity and diversity into board and senior role appointments.

☑️ WHAT NEXT?

The future hydrogen transmission network operators shall adopt and publish, by early July 2025, the final statutory documents, taking into account the Commission’s and ACER’s opinions.